The pandemic changed tech M&A forever. In the work from anywhere world, there are more buyers globally with more cash than ever, but the biggest change is the pace. It has quickened to literally a real-time process. And with more pre-emptive offers, you need to be careful as record prices are being paid. Let me explain…

In the old days, remember 2019? My friend, Robert, a Private Equity fund executive could take a vacation, letting you know he'd respond to your opportunity in a couple of weeks. Now, when he's on holiday, he has to have his iPad at the ready, responding while the kids are asleep.

He doesn't like this change. Definitely not. First off, he has to deal with more bidders. Second, he doesn't have the time he'd like to work the seller into a structured deal with targets and earnouts. Third, the deals are being pushed towards all cash with multiple bids.

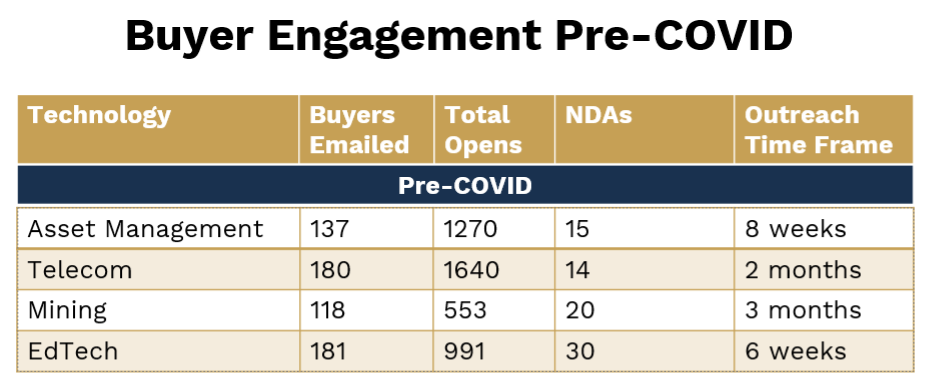

I've broken down some response statistics into pre-COVID and post-COVID transactions to show you how radically things have changed. You can see how much longer the early group took to get a meaningful response. Let's look at four examples in asset management, software telecom, mining, and EdTech. We show four columns, the first being number of buyers, the second being number of opened emails regarding the opportunity, the third being number of NDAs, and the fourth being the time it took to get into meaningful dialogue with competitive bidders. So, for example, reading across that first one, Asset Management, 137 buyers, 1,270 opens, 15 NDAs in eight weeks.

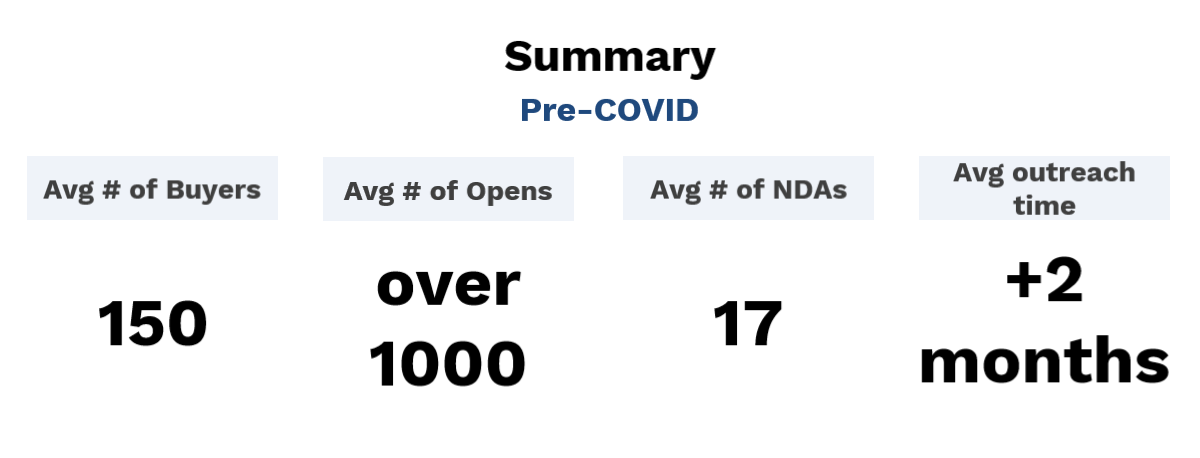

We look at the summaries and the average number of buyers—about 150. The number of opens—just over a thousand, the number of NDAs averaged about 17. And then the outreach time to get to meaningful dialogue was two months plus.

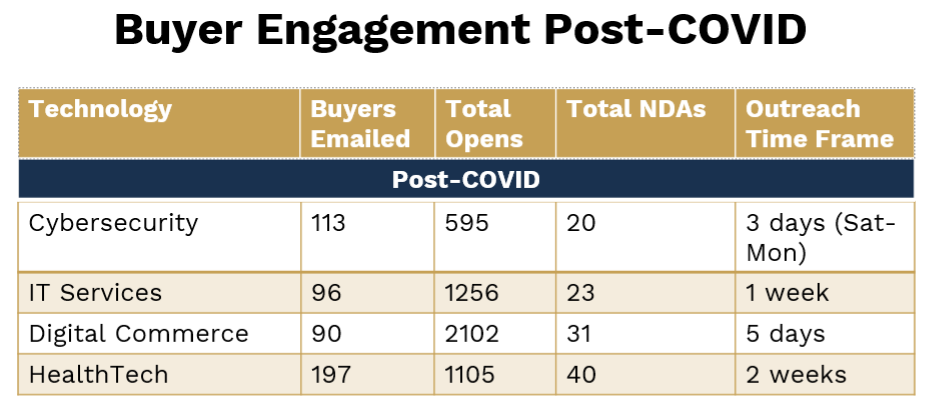

Now let's look at the post COVID deals done in the last few months when discussions were virtual. Here, we've picked four companies—Cybersecurity, IT Services, Digital Commerce, and Healthtech. Let's go through the same exercise. The Cybersecurity company had 113 buyers targeted, 595 opens, 20 NDAs, and only three days to get a response from Saturday to Monday. It was very hot company.

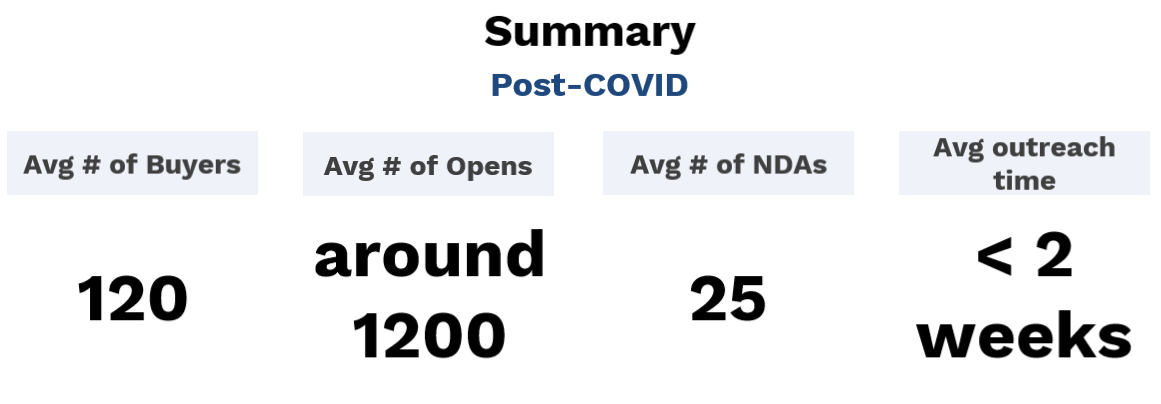

Again, going through our same summary, we had somewhat fewer buyers, an average of about 120, mostly due to the size of the deals. The number of opens was around 1200. The number of NDAs was around 25—up dramatically—buyers wanted to know more right away. The biggest change was the amount of time it took to get to meaningful dialogue—just a little over a week! That's stunning relative to over two months pre Covid!

That's why we say this is basically a real-time bidding process today. Remember my friend, Robert, the PE—if he's not involved in getting back to you immediately, he's out of a job. At the outset, I mentioned record prices because there's so many bidders, including SPACs, which you can learn more about in April's webcast available on-demand.

Case Studies

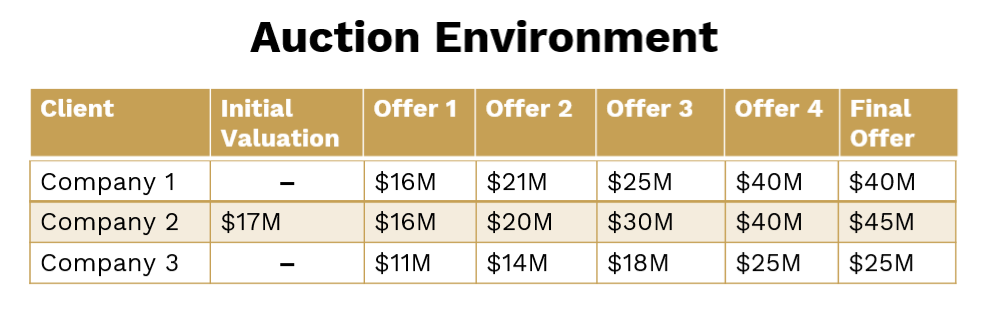

Now, let's take a look at three examples of companies that recently sold. There was an initial pre-emptive offer in each case, and all of them had multiple bidders, multiple offers. The first company, the first offer was $16M—a preemptive offer, with horrible structure. Through a competitive process, we moved from $21M to $25M. Finally, it jumped up to $40M.

In case study two, an international client, small company, $3M. Initial valuations around $17M. First offer was $16M, the second offer was $20M, the third offer was $30M, and then $40M. Finally, just before we signed the LOI, and finally, $45M.

In case study three, it's a Healthcare client. The initial pre-emptive offer was $11M, which we quickly moved $14M, then $18M. The final offer was $25M.

In these case studies, particularly the first two at over $40M, you can see the impact of creating competitive tension through an auction process with the buyers—greed and fear are the dominant emotions in tech M&A. It's wonderful if the buyers buy you, but terrible if they don't because they may lose you to a competitor. That's why you saw the prices in these first two examples jump up to over double.

As I mentioned, in each of these cases, the first offer was a pre-emptive and in each of them the client seriously considering accepting the offer. These results are obviously better than the normal 48% improvement we see on average from first to last offer which we talk about in our conferences. We also mention in our educational events that 75% of the time, there will be another bidder that will pay more—25% of the time it's someone you've never heard of. And in each of these, the final buyer was not the first bidder as the one for $45M didn't get through due diligence, so we closed with backup the backup offer at $40M—just another reason to do a global search.

But to get these results, it means you must be much better prepared, have your ducks in a row. With the pace today, you need to know what questions the buyers are going to ask, have the answers and be able to provide follow-up materials immediately. If buyers are going to spend the effort and resources to respond professionally…this fast...then they expect the same from you. So more than ever, the preparation stage means needs to be done right. Or you won't get an offer, let alone that optimal outcome you deserve. And remember, buyers give you only one shot. It's hard to go back to them.

From Corum's perspective, even though we sold have sold more tech companies than anyone, we had to respond to this warp-speed pace with even greater preparation of our clients. We added more global staff to each Client preparation meeting (IPM), most former tech CEOs who've sold their company.

Further, we added an additional layer of executive coaching before actual presentations. Even though we have by far the largest, most comprehensive buyer database—there are so many new buyers, new players, that we increased our research get to the right people in the right companies, and lastly, we increased our writers involved in each engagement, to ensure that the executive summary, your story, best maps your technology—your opportunity—to what the buyers are telling us they want.

And as you can see from these results, it's really paying off. We're attracting more buyers with multiple bids for record valuations. Getting quotes like this every week:

"I have personally suffered through bad service from major M&A firms in NY, Boston and Silicon Valley during my own career—so, I want to acknowledge both the work and the patience your teams have exhibited in the process." Corum Client

Closing Thoughts

First, we are seeing more pre-emptive bids—often from bottom feeders that know they'd be priced out in a competitive situation. You know, it's flattering to get such offers. It's easy to think, "Do I really need to go through the process of going to market?" It'd be so easy to just say yes. Besides, the offer will expire. It's the old bird-in-the-hand mentality. When it comes to those first pre-emptive bidders, the best advice is an old line from the war on drugs, "Just say NO!"

Too many sellers these days are leaving over half their value in the table because they took poorly structured transactions in deals where the liability and tax were biased towards the buyer. You deserve better after years, even decades, of building your company. Don't make a decision you'll regret the rest of your life.

The second closing comment is that now, more than ever, it's important to get educated before diving into the M&A process. It's absolutely necessary with today's frenzied pace. Thus, I would encourage you to attend one of our online seminars: Merge Briefing—an excellent overview of the tech landscape and sale process, one of the Growth and Exit Strategy events, Succession Planning, or if you're really serious, attend our half-day executive bootcamp—Selling Up Selling Out. It is the most attended tech executive conference in history running every week since 1990 and is updated quarterly.