France has a vibrant technology scene with a well-educated tech talent pool, world-class STEM universities and Grandes Ecoles, and innovative tech firms. French Tech companies leverage these resources and stand out with sophisticated technology products and services. They need to do so to survive the cut-throat market where the main challenge is less about developing a world-class product line and more about growing the business above a few million in annual revenues. This is one of the reasons why the typical roadmap of a French tech firm will often include an M&A exit.

Being the second largest European economy, France has a sizable tech M&A market with about 100 transactions per year. By number of deals, the French tech M&A market is comparable to that of Germany or the Benelux. However, in value terms, the French market is smaller than these other markets. Its median deal value was €12M in 2017 compared to €40M for the German market and €70M for the Benelux one.

Trends In Line With The Global Tech M&A Market

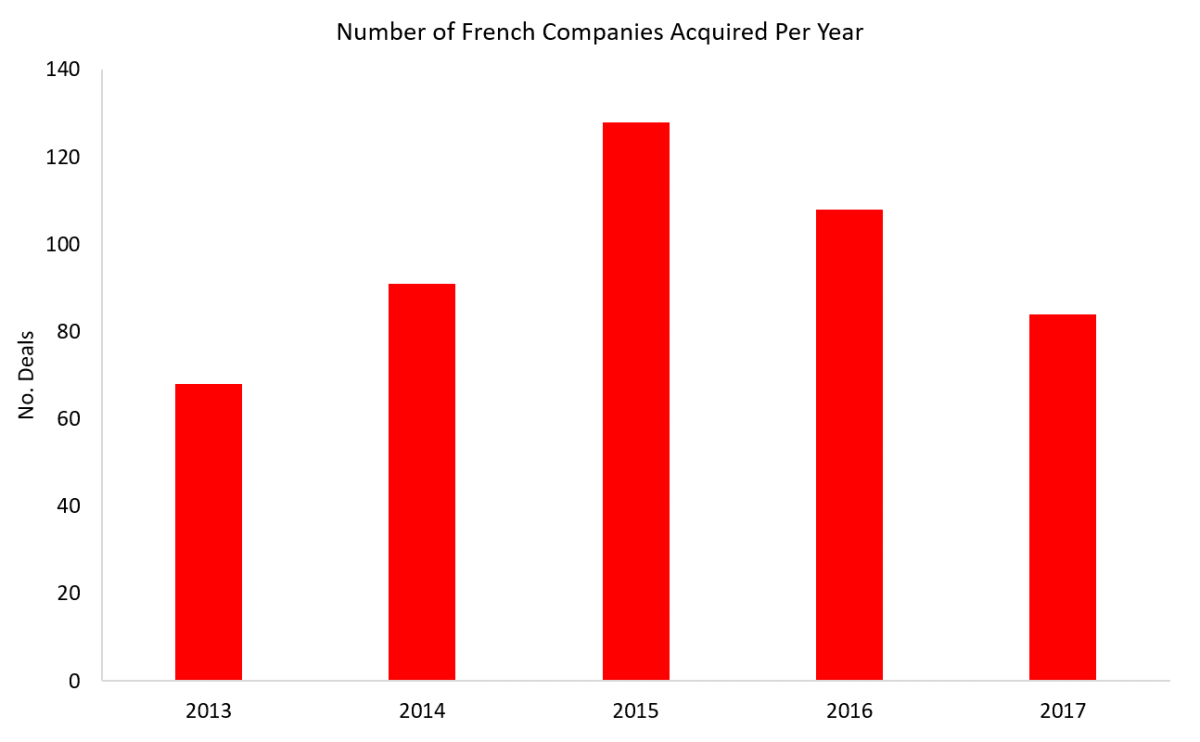

Like the global M&A market, the number of acquired French tech firms hit a peak in 2015 and decreased subsequently as supply began to run low.

Source: 451 Research, Corum Research

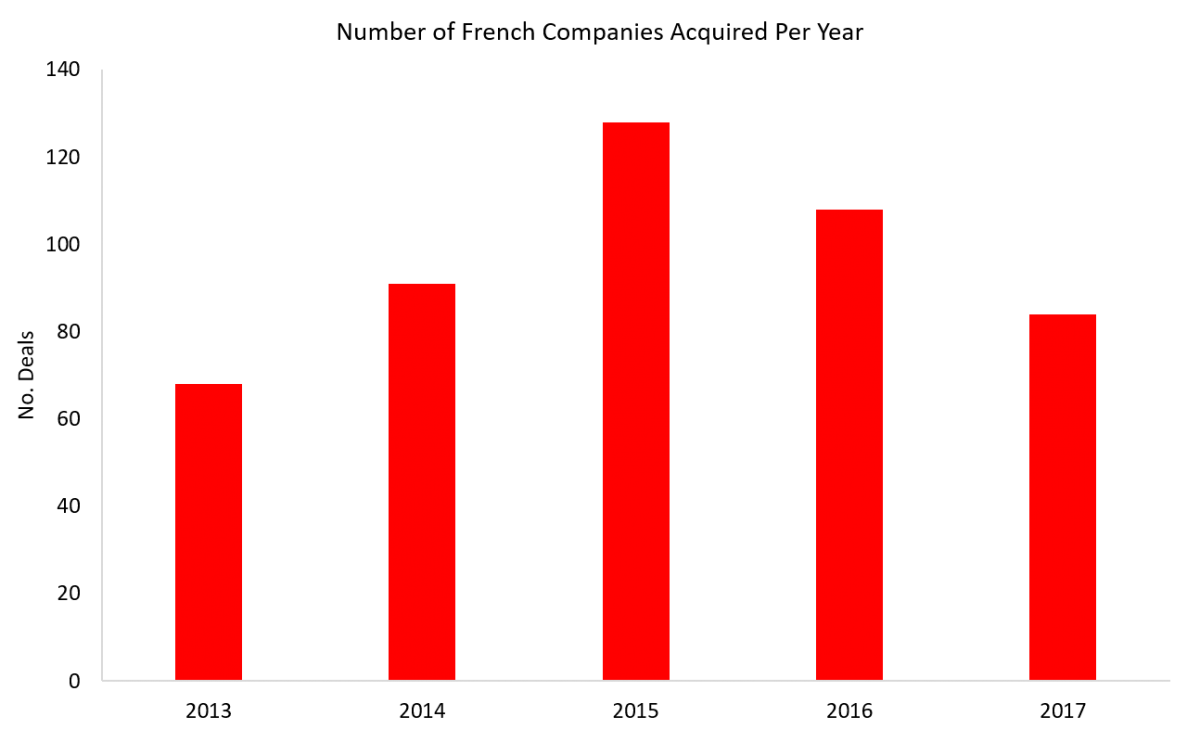

However, the number of acquisitions made by French acquirers held steady through 2016 and even showed a slight increase in 2017 driven by an unabated appetite for tech acquisitions from buyers across sectors.

Source: 451 Research, Corum Research

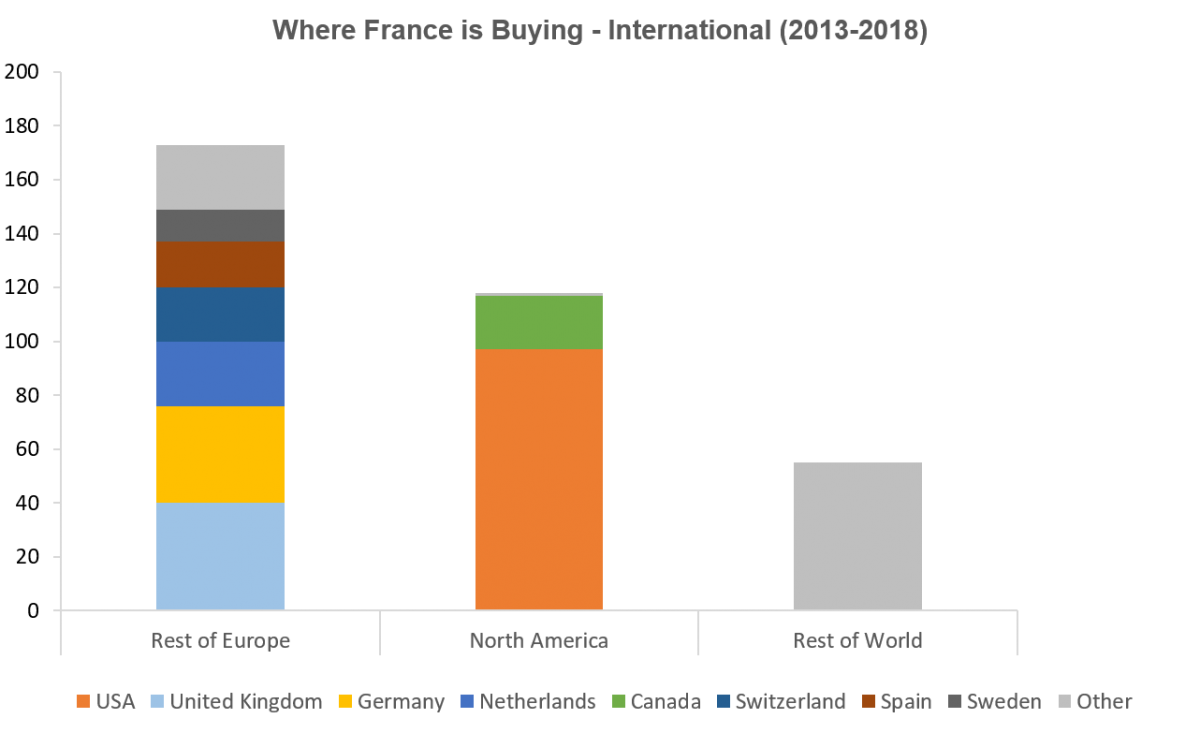

With a gargantuan appetite for international technology and growth, French buyers went out of their way and made about 62% of their acquisitions outside France. That means that they have the skills, sophistication, and financial resources required to outbid their international competitors.

The main acquisition destinations for French acquirers are within the European Union. In particular, the biggest destinations have been the UK, Germany and the Netherlands. However, the United States remains the main country for French tech acquirers, as can be seen in the chart below.

Source: 451 Research, Corum Research

French acquirers would be keen to acquire even more US tech firms and expand in the US market. The reason they did not do so has less to do with high valuations and more with concerns over staff retention. This is particularly true for areas such as Silicon Valley where tech talent is in strong demand.

Who Buys French Tech Firms?

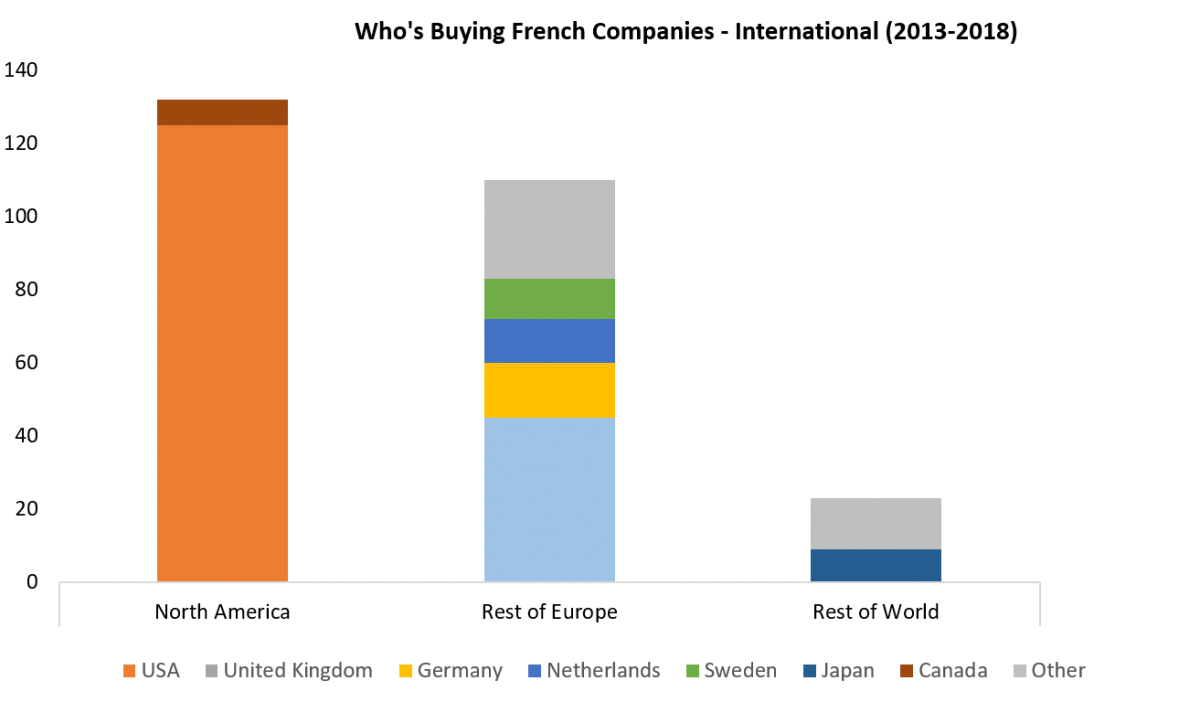

On the buy-side, the majority (55%) of French companies are acquired by foreign firms. This underscores the need for French sellers to set up a global selling process and reach out to all potential buyers in the US, Europe, and Asia. That can only increase the valuation of the sellers by increasing the number of potential buyers and therefore the relative negotiation power of the sell-side.

Source: 451 Research, Corum Research

The US remains the main acquirer of French tech companies, acquiring over a quarter of these firms over the past 5 years. In Europe, we see a similar concentration as the UK, Germany, and The Netherlands together grab the lion share of acquisitions in France.

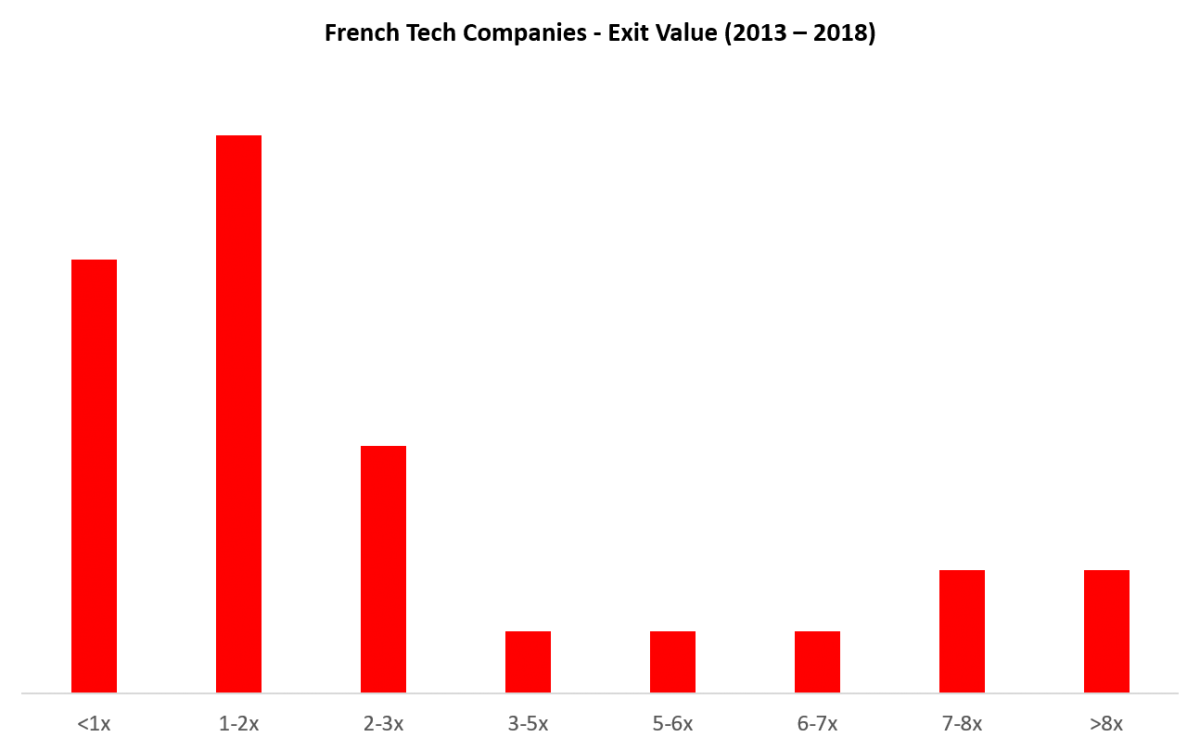

French Tech Firms Sell For Lower Prices That Comparable International Firms

When it comes to valuations, French software companies are often stuck on the low end with over half of the exits since 2013 valued under 2x revenue.

Source: 451 Research, Corum Research

The main factor that explains the relative undervaluation is the origin of the buyer. As the graph moves into higher multiples, the origin of the acquirer becomes more international. For valuations equal to or above 6x revenues, all of the acquirers are Americans. By the way, the highest multiple in our sample is equal to 19x revenue.

A few Recent French Tech M&A Transactions:

- Wright Medical Group from the Netherlands acquired IMASCAP for $62.5M in December of last year to add its 3D shoulder surgery technology to Wright’s suite of implanting inventory.

- FactSet Research Systems, a US firm, bought BISAM in March 2017 for just over $205M to create scale and bring BISAM’s risk systems into a broader market.

- Geolocation and logistics SaaS firm, Optilogistic, was acquired by Brazilian Maplink to drive the creation of new, more efficient solutions for its customers.

- Wolters Kluwer acquired operational risk management SaaS firm Enablon to advance further into the global compliance market.

- Canadian network monitoring and analytics solutions provider EXFO acquired mobile operator customer experience SaaS firm Astellia for about $32M to help operators keep pace with a quickly changing industry and to deploy infrastructures in the 5G disruptive trend.

- FoodChéri was bought by Sodexo in another trend-driven bricks-to-clicks Composite Commerce deal.

- The top acquirer of French companies, Claranet, acquired IT infrastructure services provider Diademys to expand and strengthen its international footprint.

- Germany’s CENIT acquired product lifecycle management software solutions provider Keonys for $6.5M to complete its PLM solution portfolio.

Conclusion

On the buy-side, French acquirers are keen to buy tech firms abroad and did so in 65% of their deals over the last five years. This implies that they have the financial resources to out-bid international buyers.

French Tech sellers have the technology skills to come up with world-class disruptive technologies and already attract the attention of international buyers with 55% of French companies sold to an international acquirer.

But French sellers tend to exit for lower multiples than international comparable companies, in particular when they are acquired by local buyers. Over the last five years, the French transactions that stand out with a high-valuation (above 6x revenues) all have an international acquirer, a US one in particular.

Sellers should set up more often an international process that brings international potential buyers to the negotiation table. That can only increase the value of exits, at least up to international standards.

For more detailed information, please listen to the French Tech that I participated in for WFS.