March 26, 2024

Cow Corner has Acquired Controlling Interest in Corum Client Glider

by Corum Group

by Corum Group

March 4, 2024

Insights from Corum Dealmaker Rob Wellman

by Corum Group

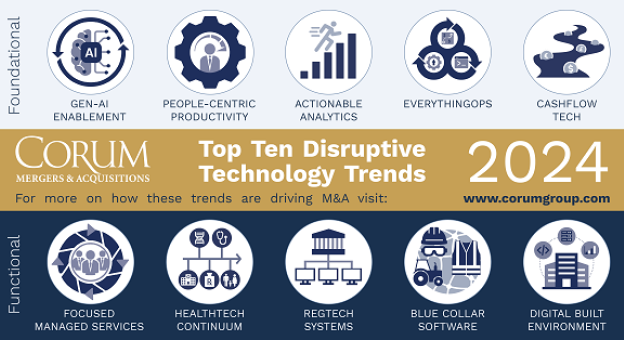

January 28, 2024

2024 Top 10 Disruptive Tech Trends

by Timothy Goddard

by Timothy Goddard

January 7, 2024

The Closing Statement – What You Need to Know

by Corum Group

January 3, 2024

Major Tax Changes for US Software Companies

by Callum Turcan

by Callum Turcan

December 11, 2023

Dura Software Acquires Infinity Software Holdings

by Corum Group

December 5, 2023

Merger-Market Fit

by David Levine

by David Levine

December 4, 2023

Peoplesafe Expands Global Reach with Acquisition of Corum Client OK Alone

by Corum Group